A few weeks ago, the International Federation of the Phonographic Industry reported that the Japanese music industry saw a decline of 2.1% in 2020, its second consecutive year of decline. The Recording Industry Association of Japan recently released its year end report for 2020, going into more detail about the state of the industry over the course of last year.

The COVID-19 pandemic greatly affected the Japanese music industry last year. Despite what the IFPI reported, the RIAJ reported that the combined physical and digital markets saw a decline of 9% in 2020, to ¥272.7 billion, the second year in a row of decline.

In 2020, the revenue of the physical market, which includes CDs, vinyl, DVDs, and Blu-rays, decreased by 15% to ¥194.4 billion, the second consecutive year of decline. Last year also saw a 19% decline in the number of units produced compared to the previous year, totalling 146.34 million units.

On the other hand, the revenue of the digital market, which is composed of downloads and streaming, increased by 11% compared to 2019, totalling ¥78.3 billion. This is the seventh consecutive year of growth, and the third consecutive year of double digit growth.

In regard to music audio discs, the number of units produced fell by 21% compared to 2019 to 156.7 million units, while revenue from this segment decreased 15% to ¥129.9 billion. The number of CD albums produced fell by 20% to 71.29 million units, while their revenue fell by 15% to ¥96.3 billion. In terms of CD singles, the number produced declined by 25% to 32.64 million, while their revenue fell by 15% to ¥30.6 billion. The vinyl market saw its first year of decline after sixth consecutive year of growth. This segment saw a decrease in the number of units produced of 10% to 1.1 million units, while revenue fell by 1% to ¥2.1 billion. Domestic music made up 91% of revenue, with international music making up the remaining 9%. In 2019, the make up was 90% domestic and 10% international. The share of revenue of domestic music in 2020 is the highest it’s been in the last 10 years.

In terms of music video discs, the number of units produced decreased by 12% compared to the previous year to 40.67 million, while shrank grew by 15% to ¥64.5 billion. The number of DVDs produced declined by 15% to 26.98 million units, while revenue dropped by 22% to ¥30.6 billion. In regards to Blu-rays, the unit production fell by 7% to 13.69 million units, while revenue fell by 8% to ¥34 billion. This decline for Blu-rays comes after two years of consecutive growth for both unit production and revenue.

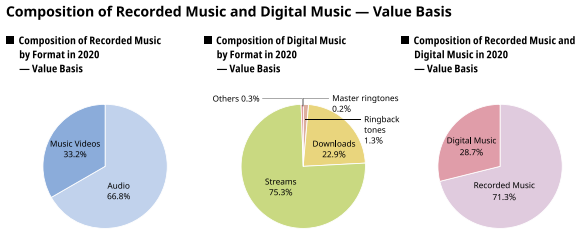

Based on revenue, the physical market is 66.8% audio discs and 33.2% video discs.

When it comes to the digital market, downloads fell by 21% in 2020 compared to the previous year to 74.35 million downloads. Download revenue fell by 20%, to ¥17.9 billion. On the other hand, streaming grew by 27%, to ¥58.9 billion. Based on revenue, the digital market is 75.3% streaming, 22.9% downloads, 1.3% ringback tones, .2% master ringtones, .3%.

In terms of total revenue, the Japanese market is 71.3% physical and 28.7% digital.

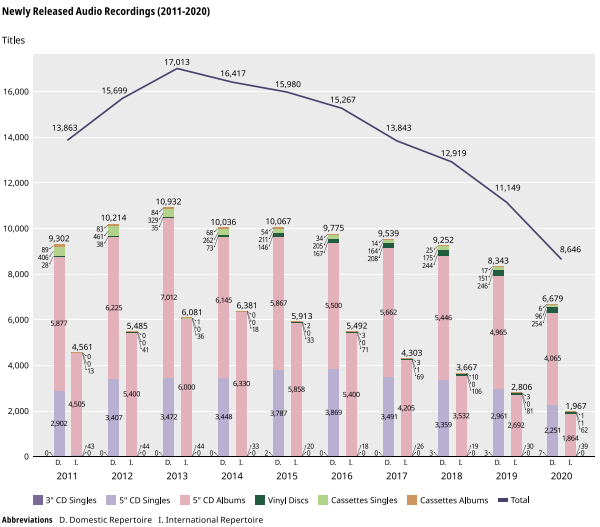

There were 8,646 newly released physical recordings last year. This is the seventh year of decline, with the last year of increase being 2013’s 17,013. The number of newly released physical recordings in 2020 is the lowest its been since about 1965.

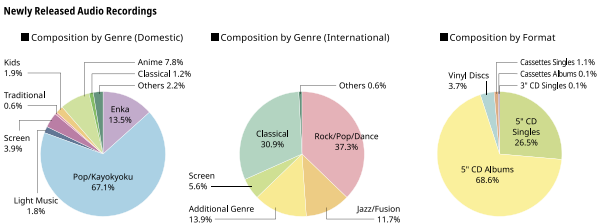

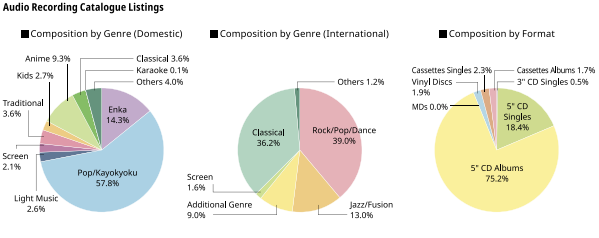

Pop / kayokyoku is the most popular genre for newly released domestic physical recordings in 2020, comprising 67.1% of the market. It is followed by enka (13.5%), anime (7.8%), screen (3.9%), kids (1.9%), light music (1.8%), classical (1.2%), traditional (.6%), and miscellaneous (2.2%).

Rock / pop / dance is the most popular genre for newly released international physical recordings last year, making up 37.3% of the market. It is followed by classical (30.9%), additional genre (13.9%), jazz / fusion (11.7%), screen (5.6%), and miscellaneous (.6%).

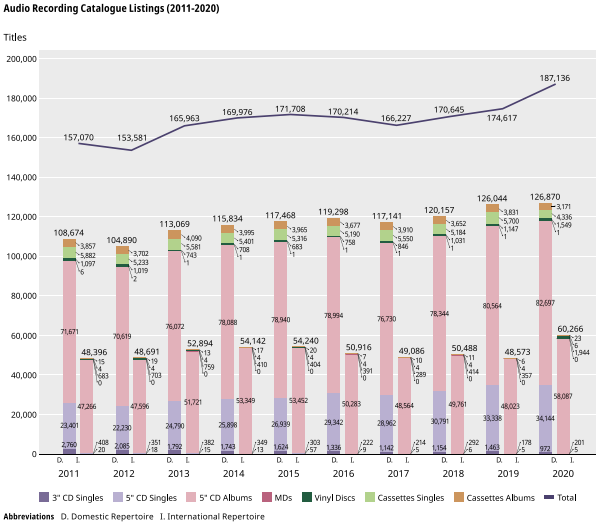

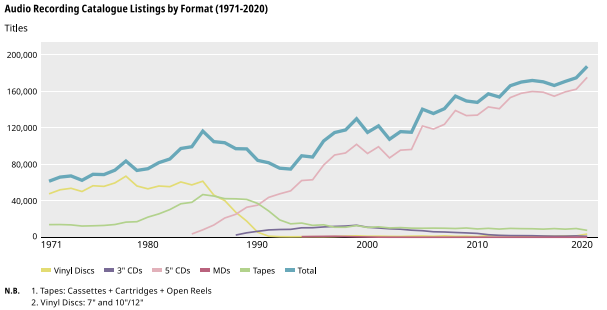

There were a record 187,136 catalog (old and new music combined) listings last year.

Pop / kayokyoku is the most popular genre for domestic catalog listings in 2020, comprising 57.8% of the market. It is followed by enka (14.3%), anime (9.3%), traditional (3.6%), classical (3.6%), light music (2.6%), kids (2.7%), screen (2.1%), karaoke (.1%), and miscellaneous (4%).

Rock / pop / dance is the most popular genre for international catalog listings last year, making up 39% of the market. It is followed by classical (36.2%), jazz / fusion (13%), additional genre (9%), screen (1.6%), and miscellaneous (1.2%).

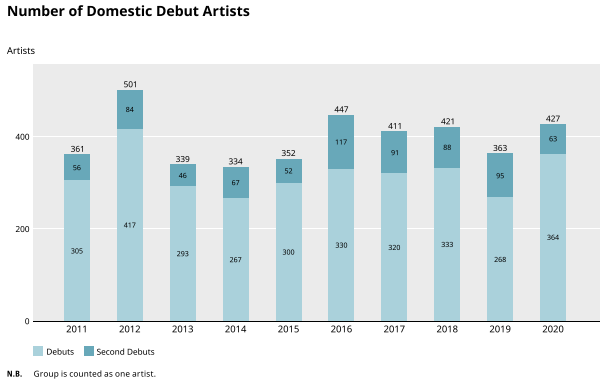

There were 427 debuts last year, made up of 364 first debuts and 63 second debuts.

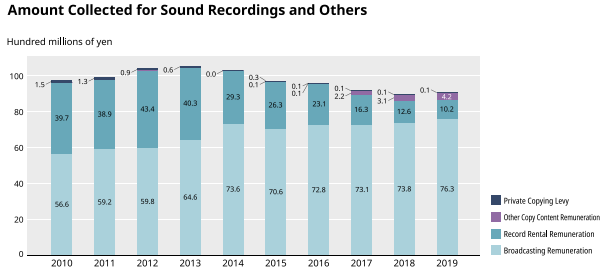

There were 1,727 record rental shops in 2020. This is the same number that existed in the early 1980s. Record rental shops have been in decline since their peak in 1989 at 6,213.

The revenue lost by the decline of record rental shops has gradually been replaced by revenue from broadcasting.

The full report can be read here.